Choosing the right finance structure for your business car loan can significantly impact your cash flow, tax position, and overall business finances. Australian businesses have three main options when financing commercial vehicle loans: chattel mortgage, lease, and hire purchase. Each structure works differently and suits different business situations.

As a trusted finance broker, NeuLoans helps Australian businesses navigate these options and select the structure that best matches their needs. We work with leading lenders including Westpac, Latitude, FirstMac, and Morris Finance to provide tailored business vehicle finance solutions.

This guide breaks down each option in simple terms, explaining how they work, their advantages, and which business situations they suit best.

This information is general in nature and does not constitute financial advice. Consult your accountant regarding tax implications.

Understanding the Three Main Options

Before diving into details, here’s a quick overview of each commercial vehicle loans structure:

Chattel Mortgage

A chattel mortgage means you own the vehicle from day one, and it acts as security for your loan. This is the most popular option for established businesses with GST registration.

Finance Lease

With a finance lease, the lender owns the vehicle throughout the lease term. You use the vehicle for business purposes and have options at the end of the lease period.

Hire Purchase

Hire purchase sits between the other two options. You use the vehicle throughout the loan term, but ownership only transfers when you make the final payment.

Chattel Mortgage: Own It From Day One

Chattel mortgage is the most common business vehicle finance structure in Australia.

How Chattel Mortgage Works

- You purchase the vehicle using borrowed funds

- The vehicle is registered in your business name

- You own the asset immediately

- The lender holds a mortgage (security interest) over the vehicle

- You make regular repayments over the agreed term

- At the end, you can choose to keep the vehicle or sell it

Key Features

Ownership: Immediate ownership means the vehicle appears as an asset on your business balance sheet from day one.

GST Benefits: If your business is GST-registered, you can claim the GST paid on the vehicle purchase price back in your next Business Activity Statement (BAS).

Tax Deductions: You can claim depreciation on the vehicle value and deduct interest paid on the loan as business expenses.

Balloon Payments: Option to include a residual value (balloon payment) at the end of the term, reducing regular repayments.

Flexibility: You control the asset and can sell it if needed (subject to paying out the loan).

Who Chattel Mortgage Suits

Chattel mortgage works best for:

- GST-registered businesses

- Established companies with steady cash flow

- Businesses wanting immediate asset ownership

- Companies seeking maximum tax benefits

- Businesses planning long-term vehicle retention

Advantages

- Immediate ownership and control

- GST claim on purchase (if registered)

- Depreciation and interest deductions

- Flexibility to sell or modify vehicle

- Clear asset ownership for balance sheet

Considerations

- Requires business ABN and trading history

- Vehicle value appears as business asset

- Responsibility for all maintenance and running costs

- Commitment to ownership

Finance Lease: Maximum Flexibility

Finance leasing offers a different approach where the lender retains ownership.

How Finance Lease Works

- The lender purchases the vehicle

- You lease it for an agreed term

- You have full use of the vehicle for business

- You make regular lease payments

- At lease end, you have three options:

- Purchase the vehicle at residual value

- Return the vehicle

- Refinance and continue leasing

Key Features

Ownership: Lender owns the vehicle throughout the lease. It doesn’t appear as an asset on your balance sheet.

Tax Treatment: Lease payments are typically fully tax-deductible as business expenses.

End Options: Flexibility at lease end – buy, return, or refinance.

Maintenance: Often includes maintenance packages (though not always).

Upgrades: Easier to upgrade to newer vehicles at lease end.

Who Finance Lease Suits

Finance leases work well for:

- Businesses wanting flexibility

- Companies preferring not to own depreciating assets

- Businesses that regularly upgrade vehicles

- Companies managing balance sheet appearance

- Businesses wanting predictable payments

Advantages

- No asset ownership commitment

- Full lease payment deductibility

- Flexibility at end of term

- Easier vehicle upgrades

- Off balance sheet financing

Considerations

- No ownership during lease

- Must return vehicle or pay residual to keep

- Less control over the asset

- May have mileage restrictions

- Typically higher total cost if purchasing at end

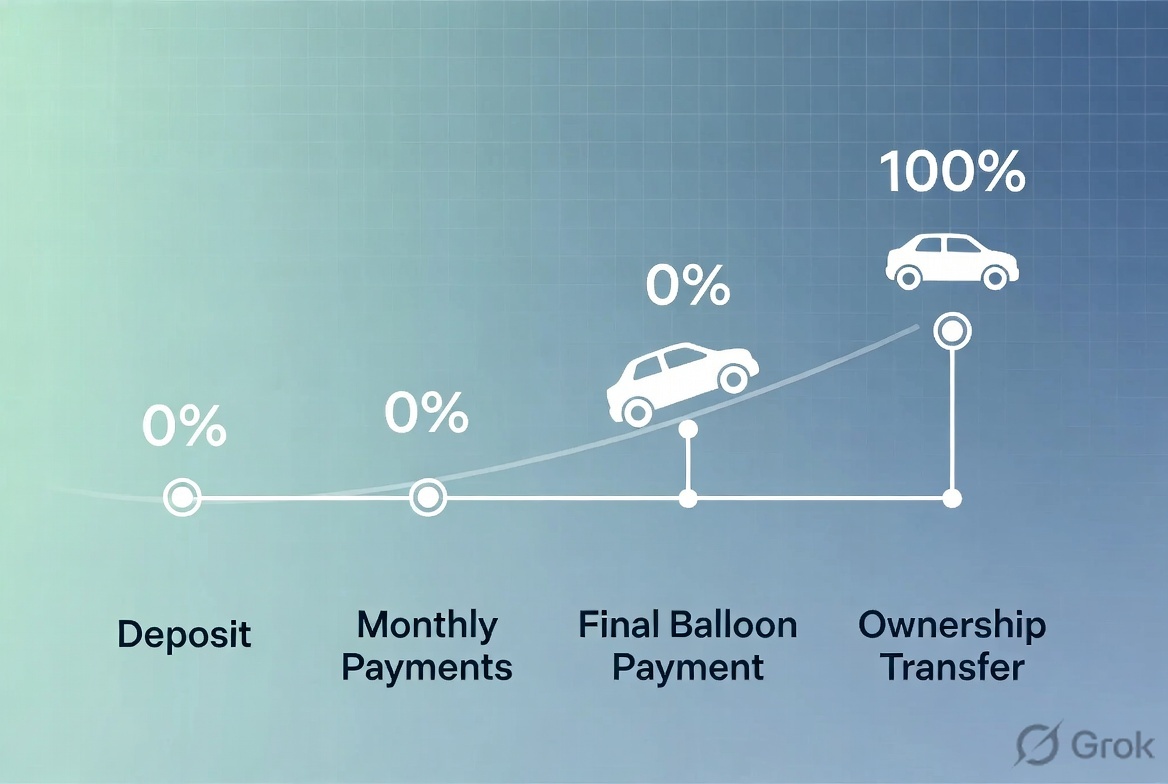

Hire Purchase: Gradual Ownership

Hire purchase combines elements of both chattel mortgage and lease.

How Hire Purchase Works

- The lender purchases the vehicle

- You hire it for business use

- You make regular payments over the term

- Ownership transfers when you make the final payment

- No large balloon payment required (usually)

Key Features

Ownership: Delayed ownership – you own the vehicle only after the final payment.

Security: Vehicle acts as security for the agreement.

Tax Treatment: You can claim depreciation and interest deductions (similar to chattel mortgage but without GST input credit).

No Balloon: Typically structured without residual values.

Simple Structure: Straightforward arrangement with clear ownership timeline.

Who Hire Purchase Suits

Hire purchase works for:

- Non-GST registered businesses

- Businesses wanting eventual ownership

- Companies preferring no balloon payments

- Businesses with simpler finance needs

- Start-ups building business assets

Advantages

- Clear path to ownership

- No large balloon payment

- Depreciation deductions available

- Simpler than chattel mortgage

- Suitable for non-GST businesses

Considerations

- No GST input credit

- No ownership until final payment

- Less flexible than lease

- Commitment to full term

- Can’t sell until owned

Direct Comparison: Which Is Best?

Here’s how the three commercial vehicle loans structures compare:

Ownership Timeline

Chattel mortgage: Immediate ownership Hire purchase: Ownership after final payment Finance lease: No ownership (unless purchased at end)

GST Treatment

Chattel mortgage: Claim GST input credit (if registered) Hire purchase: No GST claim Finance lease: GST included in lease payments

Tax Deductions

Chattel mortgage: Depreciation + interest Hire purchase: Depreciation + interest Finance lease: Full lease payments

Flexibility

Chattel mortgage: Can modify or sell (subject to loan) Hire purchase: Limited until fully paid Finance lease: Return, buy, or refinance options

Balance Sheet Impact

Chattel mortgage: Asset and liability appear Hire purchase: Asset and liability appear Finance lease: Off balance sheet (in most cases)

Best For

Chattel mortgage: Established, GST-registered businesses wanting ownership Hire purchase: Non-GST businesses wanting gradual ownership Finance lease: Businesses wanting flexibility and regular upgrades

Making Your Decision

Consider these factors when choosing between chattel mortgage, hire purchase, and lease:

Your Business Structure

GST-registered: Chattel mortgage usually provides maximum tax benefits Non-GST: Hire purchase or lease may be more suitable Company vs sole trader: May affect which structure suits best

Your Cash Flow

Strong cash flow: Chattel mortgage with smaller balloon or no balloon Variable cash flow: Finance lease with predictable payments Growing business: Hire purchase for gradual ownership

Vehicle Usage Plans

Long-term retention: Chattel mortgage for ownership Regular upgrades: Finance lease for flexibility Medium-term (3-5 years): Any option works

Tax Strategy

Discuss with your accountant which structure optimizes your tax position based on your business profit, structure, and financial goals.

Asset Management Preference

Want to own assets: Chattel mortgage or hire purchase Prefer flexibility: Finance lease Building business value: Ownership options add to business assets

How NeuLoans Can Help

Choosing the right business vehicle finance structure can be complex. As a finance broker, NeuLoans simplifies the process:

Expert Guidance

We explain each option in plain language, helping you understand how they work and which suits your business situation.

Multiple Lender Access

Different lenders specialize in different structures. We access over twenty lenders, finding those offering the best terms for your chosen structure.

Tax-Aware Advice

While we’re not accountants, we work closely with businesses and their advisors to ensure the chosen structure aligns with their tax strategy.

Comparison Service

We present real options across chattel mortgage, hire purchase, and lease structures so you can compare actual terms, not just theory.

Ongoing Support

As your business grows and vehicle needs change, we’re here to help with additional commercial vehicle loans or structure changes.

Conclusion

There’s no single “best” option for business vehicle finance – the right choice depends on your business situation, tax position, cash flow, and ownership preferences.

Chattel mortgage suits established, GST-registered businesses wanting immediate ownership and maximum tax benefits. Finance lease provides flexibility for businesses that prefer off-balance-sheet financing and regular vehicle upgrades. Hire purchase offers a middle ground for non-GST businesses wanting eventual ownership without large balloon payments.

The key is understanding how each structure works and matching it to your specific business needs.

NeuLoans specializes in commercial vehicle loans across all structures. We work with major lenders including Westpac, Latitude, and FirstMac, plus specialist business lenders. Our finance broker team can explain your options, present real comparisons, and help you choose the structure that makes sense for your business.

Contact NeuLoans today for a free consultation. We’ll discuss your business needs, explain each finance structure, and present suitable options across chattel mortgage, hire purchase, and lease arrangements.

This article contains general information only and does not constitute financial or tax advice. NeuLoans is an Australian credit representative. Consult your accountant regarding tax implications. Loan approval is subject to lender criteria.